Offshore wind viability

8th December 2020

Our Zero e-Mission Future

8th December 2020Infrastructure: Enabling transport decarbonisation

Lisa Ryan and Sarah La Monaca of the UCD Energy Institute discuss whether Ireland has enough EV chargering infrastructure to address ‘range anxiety’, a recognised barrier to EV adoption.

Decarbonisation of transportation is a critical component of governments’ efforts to reduce greenhouse gas emissions in support of climate mitigation goals. Electrification of vehicle fleets, particularly in countries with ambitions to increase shares of renewable electricity supply, such as Ireland, represents a key pathway toward low-carbon mobility. Electric mobility can also help to alleviate urban air quality hazards, which are increasingly driving state and local policy action (BNEF, 2018).

Decarbonisation of transportation is a critical component of governments’ efforts to reduce greenhouse gas emissions in support of climate mitigation goals. Electrification of vehicle fleets, particularly in countries with ambitions to increase shares of renewable electricity supply, such as Ireland, represents a key pathway toward low-carbon mobility. Electric mobility can also help to alleviate urban air quality hazards, which are increasingly driving state and local policy action (BNEF, 2018).

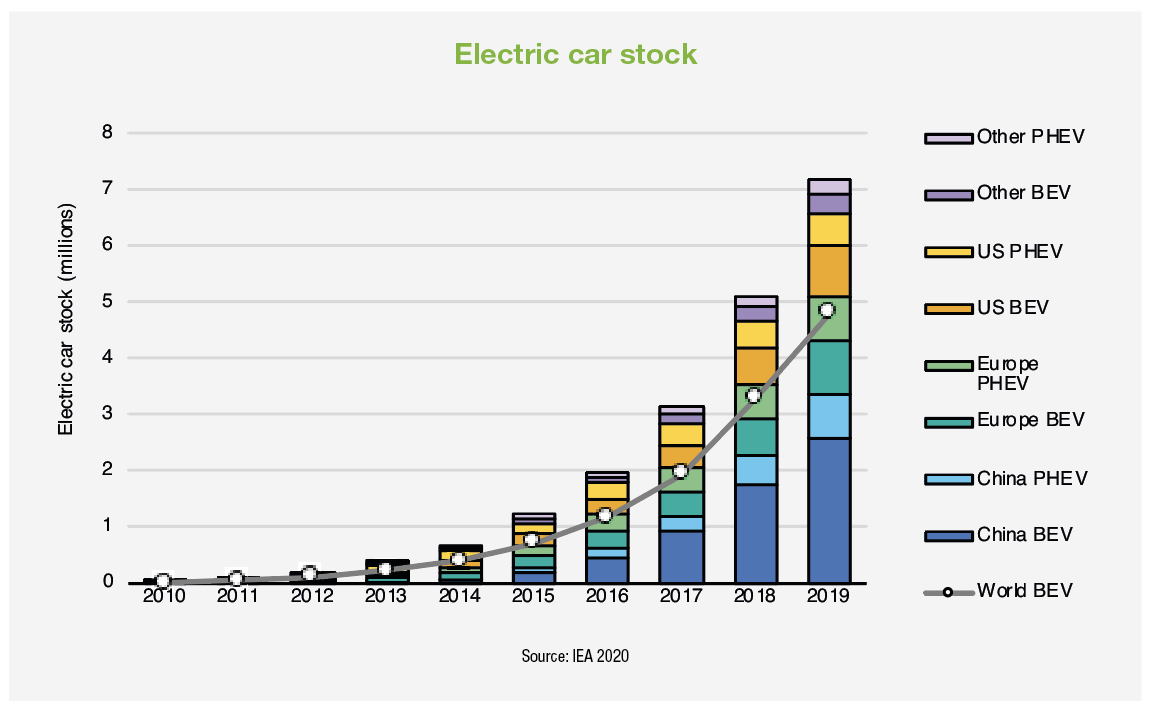

Policies aligned with these environmental objectives, as well as rapidly dropping technology costs, have led national governments and automakers to make considerable commitments to future electric vehicle (EV) deployment in recent years. Uptake has increased around the world: according to the International Energy Agency’s (IEA) Global EV Outlook for 2019, there were more than 7.2 million electric vehicles worldwide in 2019, increasing by 2.1 million on the previous year. Based on existing commitments and announced new targets, the IEA forecasts continued growth in EV market share, with a global stock of total exceeding 130 million by 2030 (IEA, 2019).

While predictions for future EV adoption point to ambitious growth, a successful transition will need to be supported by robust vehicle charging infrastructure. EV ownership requires that drivers have access to both public and home charging infrastructure so that they can feel confident in transitioning to EV ownership without fear that their driving behaviour will be curtailed due to refuelling limitations.

Some studies, such as Sierzchula et al (2014), show that countries with higher per capita public charging infrastructure are more likely to have higher shares of EVs in the national passenger car market. They show that adding an extra charging station per 100,000 residents resulted in approximately double the EV market share compared with providing an additional $1,000 in consumer financial incentives.

Here we look at the situation regarding EV charging infrastructure and whether sufficient development of charging infrastructure is underway that will reassure and encourage citizens to buy EVs.

Ireland

Successive carbon mitigation plans from Irish governments have identified the electrification of transport, and specifically EVs, as a key measure to reduce carbon emissions. Most recently, the 2019 Climate Action Plan (CAP) for Ireland proposes several actions to support deployment of electric vehicles, including maintenance and review of existing grant programmes and investment in infrastructure and behavioural change interventions.

In 2009, Ireland set a national target of transitioning approximately 10 per cent of its passenger and light commercial vehicle stock to electric vehicles by 2020, a figure which was subsequently revised to 50,000 EVs due to slow uptake (DCCAE, 2017a). The 2017 National Development Plan (NDP) renewed Ireland’s future EV deployment ambitions by setting a target of 500,000 electric vehicles on the road by 2030, with supporting charging infrastructure to follow. The 2019 CAP increased the level of ambition again to over 800,000 EVs on the road by 2030 (DCCAE, 2019).

In recent years, sales of EVs in Ireland have dramatically increased from approximately 20 vehicles only 10 years ago. This had grown in 2019 to a total of 8,473 battery electric vehicles and an additional 6,305 plug-in hybrids on the road in Ireland (DTTAS, 2020). Data available from the Society of the Irish Motoring Industry shows that 3,613 battery electric passenger cars were newly registered in Ireland in 2020 up to the end of September; plug-in hybrid electric vehicles represented an additional 2,342 passenger cars (SIMI, 2020). These numbers signify an increase of 41 per cent over the same period in 2019, which is quite remarkable given the challenging circumstances in the economy due to the Covid-19 pandemic. There are now 24 different vehicle models of battery electric vehicles and 36 plug-in hybrid models available in the Irish market (SIMI, 2020). So, while the numbers of EVs are growing significantly, huge effort is needed to reach the target of 840,000 EVs by 2030, this represents an average annual growth rate of nearly 50 per cent over the 10 years to come.

Current incentives aimed at stimulating demand for EVs take the form of cash grants to defray purchase costs, and favourable treatment on vehicle registration and road tax which improves long-term ownership costs. Consumers who purchase an EV in Ireland have been eligible for a grant of up to €5,000 since 2011; by the end of 2019, just over 17,000 vehicles had been supported by the grant (SEAI, 2020).

Budget 2021

The 2021 Budget package extended some existing supports, including the Vehicle Road Tax Relief and upfront purchase grant (worth up to €5,000 each), and a €600 grant to support the installation of a home charger. Businesses can receive a grant of up to €3,800 for electric commercial vehicles and many EVs and charging equipment are eligible for accelerated capital allowances for depreciating vehicle purchases (DCCAE, 2020). It remains to be seen whether the array of available incentives will be sufficient to achieve the huge growth in sales required.

A key factor in EV decision-making among consumers is the availability of charging options, both public and private charging stations. Quantifying prospective future EV uptake also provides some indication of what will be required from EV charging infrastructure under different adoption scenarios. The EU Alternative Fuels Infrastructure Directive (AFID) recommends that member states ensure one publicly available charger for every 10 electric vehicles. By way of comparison, Norway had approximately 9,000 public charging stations for 176,000 electric vehicles in 2017, for a ratio of approximately one charger for every 19.5 vehicles (IEA, 2018b). In fact, historically Ireland had a ratio of 1:5 of public chargers to EVs, although this was partly due to the very low number of EVs in the vehicle fleet. To comply with the AFID recommendation, Ireland would need 84,000 public chargers for 840,000 EVs on the road.

In practice, the Department of Transport stated in its 2017 Alternative Fuels Framework that the 1:10 ratio of chargers laid out in the AFID would likely never be necessary to support wide-scale EV deployment in Ireland. Furthermore, as higher capacity fast charging technology becomes the norm, public chargers will likely be able to adequately service a higher number of EVs, meaning charger ratios could be lower. In any case, it is important that Ireland set specific targets for charger buildouts which are aligned with overall EV deployment. These targets can be modified and refined as best practices for charging location, speed, and mode become better developed.

Charging network

Until 2017, the primary programme for installation of EV charging stations in Ireland was the ESB Networks’ electric vehicle pilot programme. Under the initiative, the Irish DSO, ESB Networks, was directed to spend €25 million from ratepayer network user fees to build a public charging network and deliver value through research and grid impact assessments (CRU, 2017). Execution of the programme was managed by a separate commercial entity within the ESB Group, ESB eCars. Under this programme ESB eCars installed approximately 1,100 public charging stations in Ireland, including 300 in Northern Ireland. The majority of the public charging stations are rated at 22 kW. The programme also supported 70 fast chargers in Ireland, as well as an additional 15 fast chargers in Northern Ireland (ESB, 2017b). In 2019, the Government that €20 million would be invested in fast chargers, co-funded by the Climate Action Fund and ESBN.

Few private charging companies operated in Ireland in the past and while this is starting to grow, it is difficult to estimate the number of privately owned and operated charging stations and whether they represent a comprehensive network. The dearth of commercial providers is likely not helped by the small size of the Irish market and its low EV penetration, which limit appeal to potential market entrants.

The potential for home charging may be very high in Ireland, given the various housing characteristics at large. Proximity to parking options is not currently reported under the Irish census, however the National Policy Framework for Alternative Fuels Infrastructure for Transport notes that rates of private home ownership and private parking access in Ireland are higher than other European countries, reducing the need for public charging infrastructure. In fact, this does not reflect localised conditions. Indeed, in 2016 apartments represented the most common housing type in Dublin for the first time, with 204,145 people or 35 per cent of residents living in multi-unit dwellings (CSO, 2017a). In advance of potential EU requirements for EV charging in apartment buildings, Ireland is also considering introducing guidelines that require developers to ensure new apartment buildings are EV-ready, as in the city of Westminster in London, which has implemented a requirement that all new builds and retrofits must be socket-ready to accommodate EV uptake (ICF, 2016).

In most of Ireland, people live in houses and outside urban areas the vast majority have driveways and are suitable for individual home charging facilities. For the purpose of assessing public charging infrastructure needs in Ireland, a 2016 analysis of recorded charging events at existing charging stations found that Irish EV users charged at home with the highest frequency, compared with public standard and fast-charging options (Morrisey et al, 2016).

Range and driving distances

Other geographic and demographic characteristics of Irish residents would seem to suggest suitable conditions for deployment of an efficient EV charging network. According the Central Statistics Office (CSO, 2017b), the average Irish commute is under 15km, with Dublin city (including south Dublin and Dún Laoghaire-Rathdown), Cork city, and Galway city commuters living within 10km of their workplace. These CSO data for the cities represent over one half of workers who commute by car and more than one third of total Irish commuters. Residents in Laois experience the longest commuting distances, at just over 25km. As a point of comparison, this is similar to the average urban commute in New Zealand (22km), where the Government has determined typical commuting distance as a factor that renders it well-placed for EV uptake (Ministry of Transport, 2017). Ultimately, these indicators point to a relatively high number of private car commuters in Ireland whose daily round trip car travel is well within the bounds of a typical EV battery range. Indeed, new EV models have a range of at least 400km although this degrades to approximately half this after a few years. This makes infrequent long-distance trips more difficult, as they require refuelling mid-journey. While more data is needed to better understand driver behaviour and attitudes, these longer trips appear to be more salient to prospective EV buyers compared to their typical daily driving distance.

Public perception

Despite the high number of residents with relatively short commutes, a substantial proportion of Irish drivers feel unprepared to own an EV due to a perceived lack of availability of charging: a 2017 AA Car Insurance survey found that approximately 30 per cent of respondents would be “very likely” or “somewhat likely” to purchase an electric vehicle for their next car, however, 54 per cent of those unlikely to purchase an electric vehicle attributed their hesitation to a lack of charging infrastructure (Aldworth, 2017). Future policy should accommodate the considerable variation in charging needs for urban drivers compared with rural ones. For example, a 2016 simulation of localities across the US found that available, affordable BEV technology was suitable to replace 87 per cent of vehicle-days (i.e. driving needs on a given day) without recharging. However, the vehicle-days for which BEVs fell short occurred more commonly for residents of urban areas (Needell et al, 2016). Similar determinations of range and charging requirements should be explored in Ireland.

|

Key points from UCD Energy Institute’s The State of Play in Electric Vehicle Charging Services: Global Trends with Insight for Ireland’ report • Ireland’s EV charging infrastructure has primarily been developed by a single semi-state network operator. Few additional actors have participated in this space or are active in the Irish market at all, and as a result, the competitive marketplace for charging services is underdeveloped. Future policy design should note that companies offering charging in Ireland will incur some cost for new market entry. • Despite a strong early start to national charging infrastructure deployment, the future of charging development is unclear as public charging incentives are still under development and commercial charging remains is only slowly becoming competitive. • Additional investment in and expansion of public charging networks is necessary and is essential to ensuring user confidence in a high-EV future. • The average commute for Irish drivers (less than 15 km one way) indicates that most Irish drivers’ daily needs are well within the current vehicle range. However, despite short commuting distances, a majority of people surveyed indicated that their concern over lack of charging infrastructure is a barrier to purchasing an EV. • Given Ireland’s high ratio of chargers to EVs (approximately 1:5 in Ireland compared to 1:19.5 in market leader Norway), concerns over charging access may be due to a lack of awareness about the existing network. Improved marketing and standardised road signage could direct drivers to existing chargers, or make prospective EV drivers more secure in the availability of charging resources. |

Given the relatively high ratio of chargers available for EVs in Ireland, it seems that at least some of the concern over charging access could be alleviated by awareness or marketing campaigns. As the first iteration of Ireland’s charging network was executed on the basis of ensuring nation-wide infrastructure, the next wave of installation should be better aligned with observed and likely driver profiles and network utilisation data to ensure assets are strategically sited. This may include fast-charging along major intercity corridors, as well as on-street residential charging in densely-populated cities and towns, multi-modal locations (e.g. at commuter rail stations), and car parks and retail. Specific analysis is required: Morrisey et al (2016) note that fast charging in Irish car parks received higher daily utilisation than other location and mode combinations (e.g. Level 2 charging in car parks and petrol stations, and fast-charging in car parks).

With respect to support or scepticism on behalf of the public, the IEA (2017) notes that air quality issues are a prominent issue for cities interested in EV uptake. According to the EPA data, as reported by the World Health Organisation (WHO), urban areas in Ireland that fail to meet safe levels of particulates include Galway, Dublin, Longford town, Armagh, Bray, Belfast, and Derry. The EPA notes that this is due to use of coal and peat for home heating, and to vehicle traffic (WHO, 2016; EPA, 2016). Providing support for local authorities in areas particularly affected by vehicle emissions could prove important in facilitating the rollout of EVs and corresponding infrastructure.

Dr Lisa Ryan is a lecturer in energy economics in the UCD School of Economics. She is an active member of the UCD Energy Institute where she co-leads the interdisciplinary EMPowER project relating to the decarbonisation of electricity and consumer technologies in climate change mitigation policy.

Sarah La Monaca is a former Senior Research Fellow, Energy Economics and Policy UCD Energy Institute and Senior Associate, Global Climate Finance at Rocky Mountain Institute.